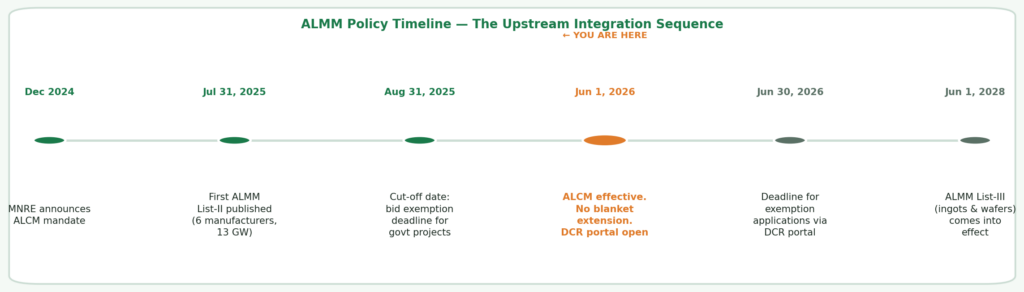

June 1, 2026 came and went — and so did any hope of a blanket extension. MNRE confirmed in its Office Memorandum of May 25, 2026 that the ALCM mandate is live. Developers who wanted more time had to file project-specific exemption applications through the DCR Portal by June 30, 2026. MNRE has categorically said they won’t accept physical applications — portal or nothing.

So here we are. If you’re evaluating solar right now — whether it’s a rooftop for your factory, an open access project, or a ground-mounted captive plant — ALCM is the new reality you’re working inside. Let’s talk about what it actually means: what will cost more, by how much, who catches a break, and what smart buyers are doing about it.

What Is ALCM — and How Did We Get Here?

ALCM stands for Approved List of Cells and Manufacturers — think of it as ALMM List-II, an extension of India’s existing ALMM framework that now reaches one layer deeper into the supply chain to cover solar cells, not just modules. For years, module manufacturers could import cells from China, assemble them in India, and sell those as “ALMM-compliant.” Technically legal. Clearly not the spirit of the policy. ALCM closes that gap. MNRE signalled this back in December 2024 — the direction was never ambiguous, just the timeline.

The Honest Supply Picture

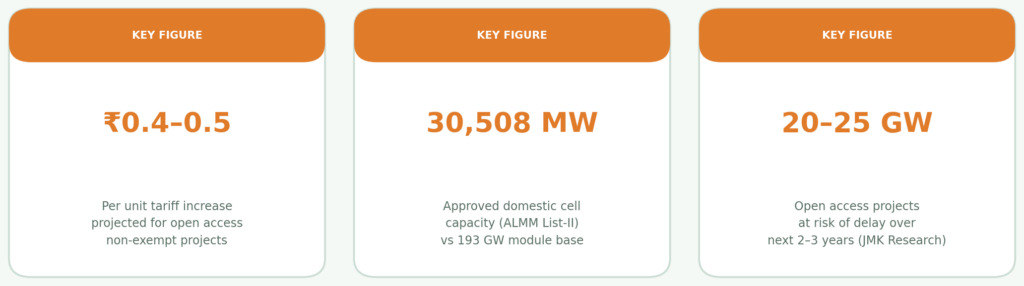

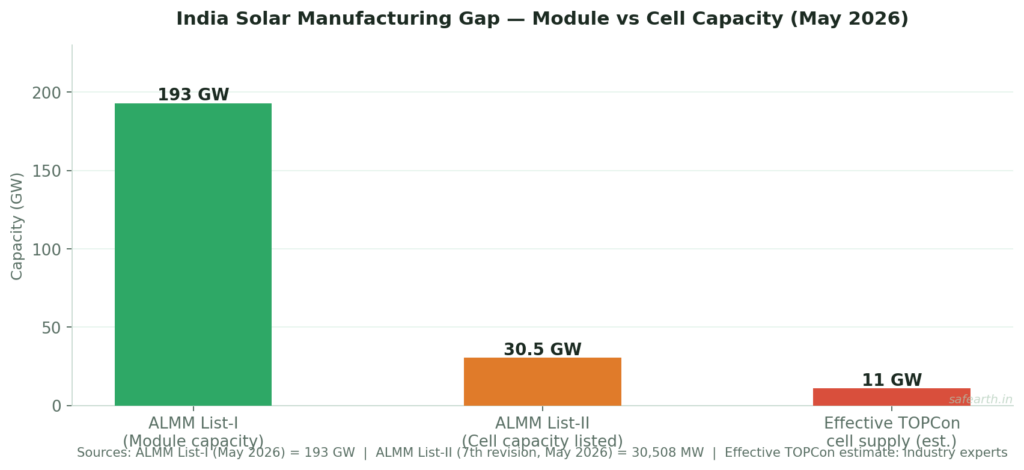

India’s module manufacturing capacity is genuinely impressive — ALMM List-I is now past 193 GW. But the whole point of ALCM is that those modules now need Indian-made cells. ALMM List-II has been revised seven times since its first publication on July 31, 2025. The latest revision puts total listed cell capacity at 30,508 MW across 13 manufacturers. That’s a 193 GW module industry trying to feed from a roughly 30 GW cell pool.

And it gets tighter. Nameplate capacity isn’t the same as cells you can actually get delivered and certified. Industry consensus puts effective stable TOPCon supply — the technology most large projects actually want — at around 10–12 GW. Cell manufacturing isn’t a fast business: specialised infrastructure, ETP and ZLD systems, 15 to 24 months of setup time. Several factories that were announced won’t come online before 2027. Meanwhile, most of India’s existing cell base is Mono PERC, and the market has largely moved toward TOPCon. The result: DCR-compliant modules are expensive and, in some cases, genuinely hard to get. Certification delays of six to nine months are being projected.

Okay — So How Much More Are We Talking?

The honest answer: it depends on your project, your state, and when you’re procuring. But here’s what the industry is saying.

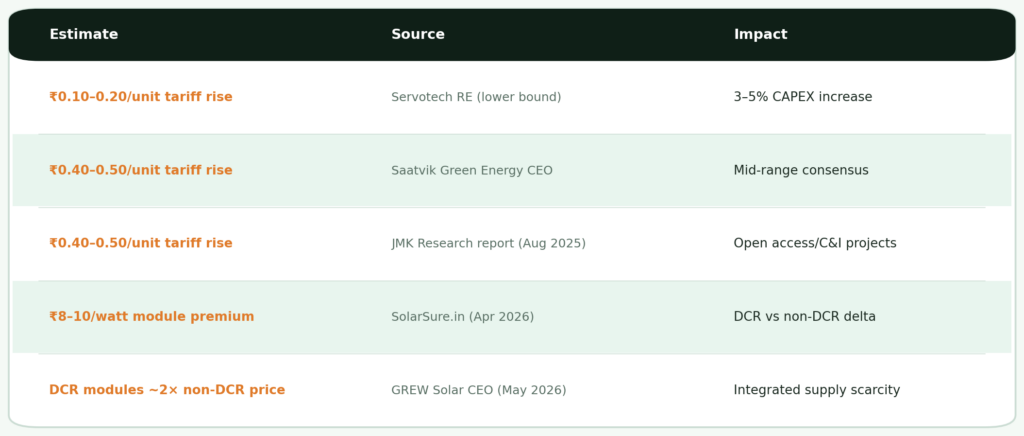

JMK Research estimates the DCR module shortage is likely to hamper 20–25 GW of green open access projects over the next 2–3 years, with project power tariffs increasing by up to ₹0.4–0.5 per unit. At the module level, DCR modules currently carry a ₹8–10 per watt premium over non-DCR. One CEO at a large module company put it plainly — DCR modules are priced at nearly double non-DCR right now.

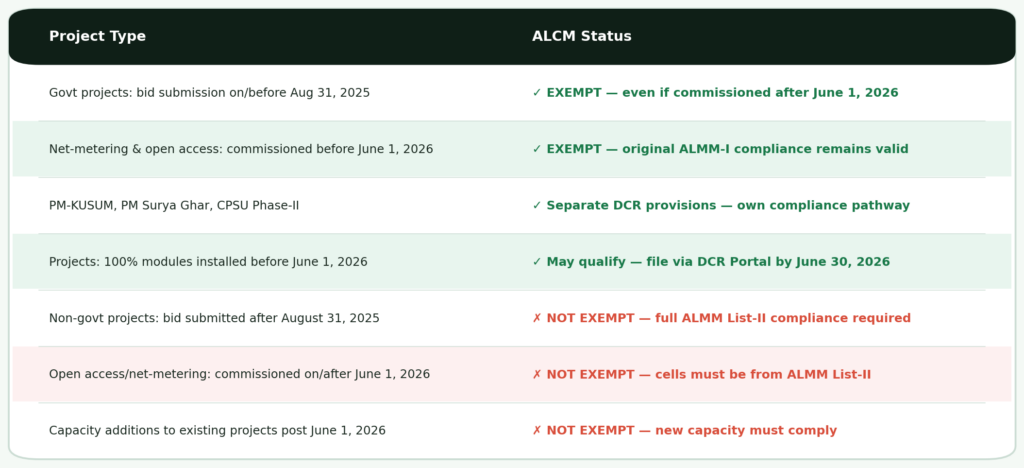

Who Actually Gets an Exemption?

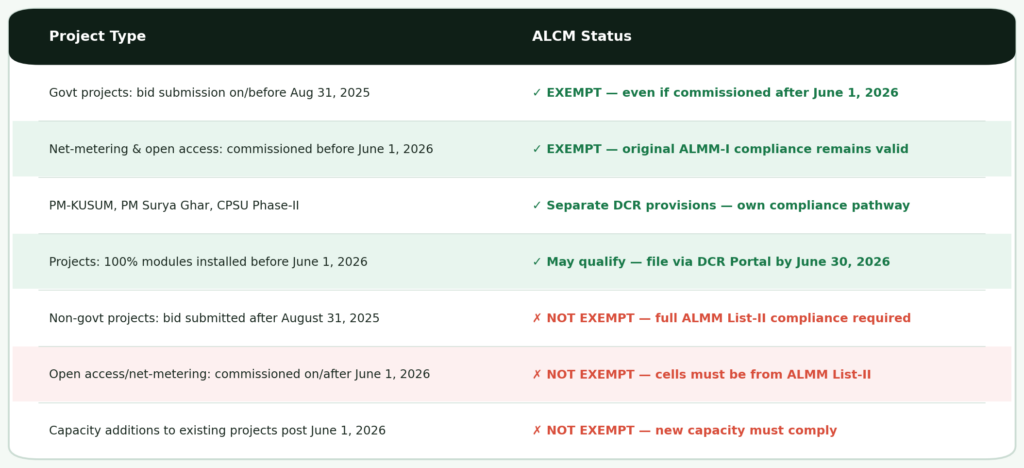

You’re likely exempt if: you’re a government project where bids closed on or before August 31, 2025; your net-metering or open access project was commissioned before June 1, 2026; you’re under PM-KUSUM, PM Surya Ghar, or CPSU Phase-II (which have their own DCR pathways); 100% of your modules were physically installed before June 1, 2026; or your project had CEIG and liaisoning approvals completed before the deadline — subject to filing documentation through the DCR Portal at solardcrportal.nise.res.in by June 30, 2026.

You’re not exempt if: you’re a non-government project where the bid was submitted after August 31, 2025; your open access or net-metering project is commissioning on or after June 1, 2026; or you’re adding capacity to an existing project after June 1, 2026. That last category covers basically the entire active C&I solar pipeline — which is exactly where most commercial and industrial buyers reading this sit. And MNRE has been clear: applications go through the DCR portal only. No physical submissions, no exceptions on process.

This Isn’t Where the Policy Stops

Worth stepping back to see the full picture. In March 2026, MNRE announced ALMM List-III — covering ingots and wafers — with a mandate date of June 1, 2028. So the upstream integration continues: modules first, then cells, then wafers and ingots. If you’re commissioning a project in 2026 meant to run for 25 years, it will be operating under the wafer mandate by 2028. That’s two years away. A DPR that doesn’t account for this is modelling a future that won’t exist.

What Should You Actually Do?

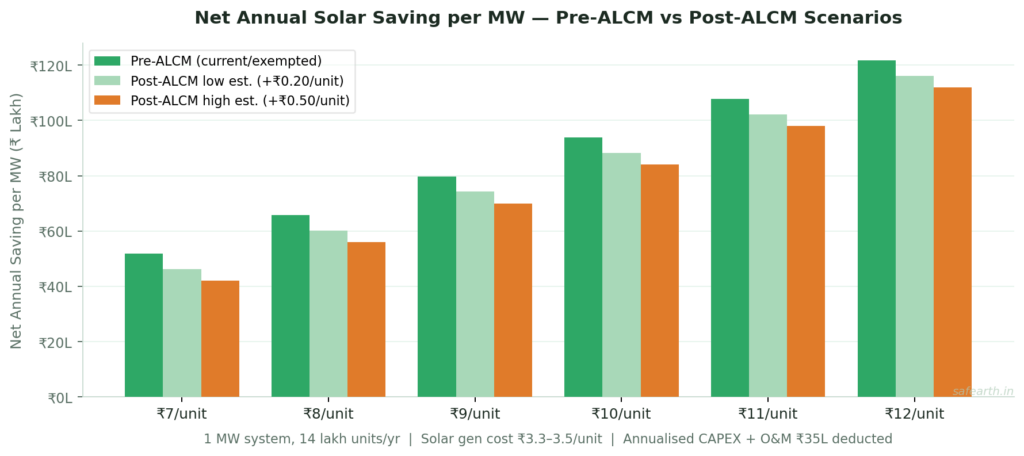

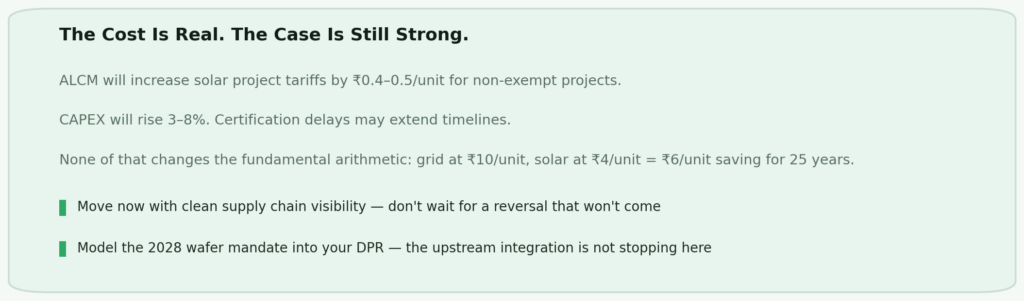

The underlying solar economics are still solid. Even with ALCM pushing costs up, a factory paying ₹10/unit to the grid and generating solar at ₹4/unit all-in is still saving ₹6/unit — compounding for 25 years as grid tariffs rise. A ₹0.40/unit ALCM impact on a ₹9/unit tariff is a 4.4% reduction in absolute saving. Uncomfortable, not catastrophic.

Move on rooftop solar sooner rather than later. The supply crunch for DCR-compliant modules is going to get tighter before it gets easier. With 20–25 GW of green open access projects competing for the same limited supply, rooftop buyers who move early are ahead of the queue.

Ask your EPC the hard supply chain question. It’s not enough to hear “we use DCR modules.” Ask which specific cell manufacturers on ALMM List-II they’re sourcing from, what their confirmed allocation is, and whether those cells carry valid certification. If they can’t answer clearly, that’s your answer. Explore SafEarth’s commercial rooftop solar advisory to understand what rigorous supply chain verification looks like.

Think seriously about the OPEX/RESCO route. Under an OPEX/RESCO structure, the developer takes on the CAPEX, the module procurement risk, and the ALCM compliance risk. If DCR module prices spike further, that pain lands on their P&L, not yours. You pay a per-unit tariff that’s below your grid rate from day one, with no capital on the table. The trade-off is you don’t build an asset and the long-term returns are lower than CAPEX ownership. For buyers who want cost reduction without procurement exposure right now, that may be worth it. SafEarth’s Capex vs PPA guide walks through exactly when each model makes sense.

Put the 2028 wafer mandate into your financial model. If you’re building a DPR today for a 25-year project, model what happens when List-III lands. It isn’t speculative — MNRE has announced it. A financial model that ignores 2028 is leaving a known risk off the table. Use SafEarth’s industrial solar ROI calculator to stress-test both scenarios.

Stop waiting for a reversal. Developers who held off expecting an extension have already paid for that decision — in delayed savings and higher equipment costs as the DCR premium widened. The policy direction is upstream integration, moving one way only. For open access solar and group captive solar buyers, the economics of acting now versus waiting are meaningfully better today than they will be in six months.

ALCM is going to cost more money. Tariffs on non-exempt projects are heading up ₹0.20–0.50/unit. CAPEX is going up 3–8%. Timelines may slip. None of that kills the case for solar. A factory paying ₹10/unit that can generate at ₹4/unit is still building a 25-year cost advantage — just a slightly smaller one than two years ago. See how SafEarth has delivered solar projects across industrial sectors at SafEarth’s case studies.